Australian Dollar

AUDCommodity-linked

M2 money supply, indexed to 2001 = 100

Every line goes up — that’s the point. Angle of attack tells the story.

All series matched through 2024; some central-bank sources lag a year or two.

AUD highlighted against the top 10 reserve currencies — M2 broad money, indexed to 2001 = 100. AUD series: IMF IFS via DBnomics, as of 2025.

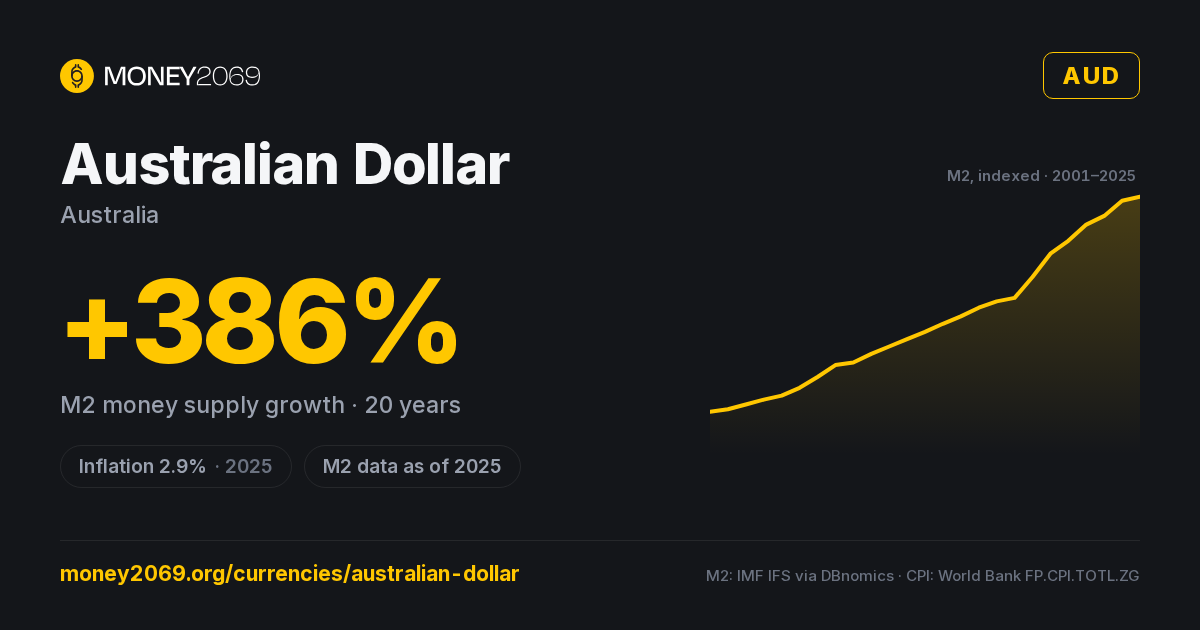

Australian Dollar M2 money supply

Broad money in AUD (cash + deposits + close substitutes), annual back to ~1960 via World Bank FM.LBL.BMNY.CN. Log scale auto-engages for hyperinflation outliers.

Australian Dollar inflation history

Annual CPI YoY since 1966 — World Bank consumer price index for Australia. Inflation volatility is one of three inputs into the Money2069 sound-money score.

{kind=link}

Purchasing power calculator

How much would your Australian Dollar be worth today if you'd held it since…?

Calculation: cumulative product of (1 + CPI YoY) from the chosen year through 2025. Source: World Bank consumer price index (annual). Daily-refreshed.

Data sources & methodology

- FX (USD):

- Frankfurter / ECB · daily, Exchange Rate API fallback

- CPI YoY:

- World Bank FP.CPI.TOTL.ZG · annual

- M2 broad money:

- IMF / central-bank monthly · World Bank annual fallback (LCU)

- Market cap (USD):

- M2 / FX rate · daily

- 10-year M2 change:

- (M2 today / M2 10y ago) − 1

- M69 score:

- Weighted: CPI (50%), 10y M2 growth (40%), 1y FX stability (10%)

- Last fetched:

- 2026-07-24 20:43:43

- Country code (ISO 3166-1):

- AUS

Note: Commodity-linked

Raw data: /api/v1/currencies/current/AUD · Rates by Exchange Rate API

The Australian Dollar from a sound-money lens

The other commodity dollar — China's iron ore proxy.

The Australian dollar is, more than any other major currency, a real-time bet on Chinese industrial demand. Iron ore alone accounts for roughly a quarter of Australian exports, with coal, LNG, and agricultural goods adding another third. When Chinese steel production rises, AUD rallies; when Beijing tightens, AUD softens.

The Reserve Bank of Australia targets 2-3% YoY inflation — slightly above the Fed and ECB — and has historically run policy a touch looser than peer central banks. Cash rate hit 0.10% in 2020 (its lowest ever), then climbed to 4.35% by late 2023 to combat post-pandemic inflation. M3 broad money roughly doubled between 2010 and 2024.

CPI peaked at 7.8% YoY in late 2022 — Australia's worst inflation in 32 years — driven by fuel, housing, and supply chain bottlenecks. By 2024 it had eased back below 4%, helped by an aggressive rate path and a cooling labour market.

The AUD's structural weakness, from a sound-money perspective, is its housing market. Roughly 65% of household wealth is locked in residential real estate, mortgages drove household debt to 200% of disposable income, and Australian banks have the most concentrated property exposure of any major banking system. That concentration is fine until the day commodity revenues fall — at which point the AUD takes the strain because the housing market structurally cannot.

Cumulative purchasing power loss since 2000: roughly 40%, or AUD 100 then = AUD 60 today.

Frequently asked questions

Who issues the Australian Dollar?+

What is the inflation rate of the Australian Dollar?+

Has the Australian Dollar been debased?+

Is the Australian Dollar sound money?+

How does the Australian Dollar compare to gold or the US dollar?+

How often is this data updated?+

Compare with

More from Money2069

The Australian Dollar inflates by policy. Money2069 runs on fixed rules — issuance targets 0%, purchasing power preserved by design, no central bank required.