Euro

EUR20-country currency union. World Bank Eurozone aggregate is empty for modern years; CPI/M2 via ECB direct feed in v2.

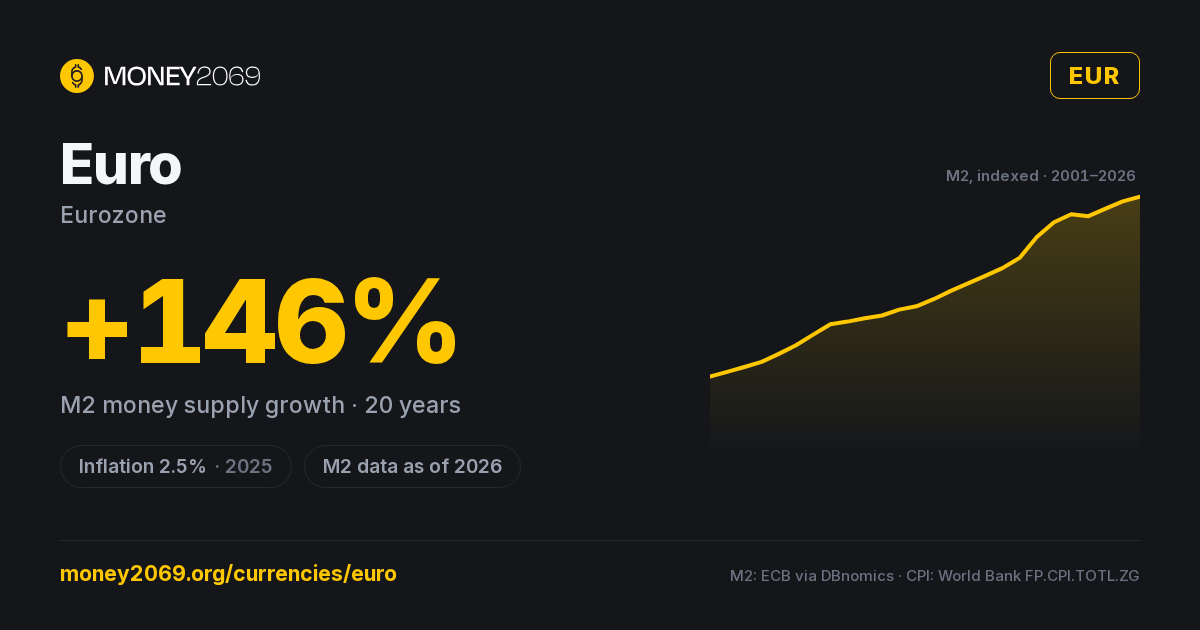

M2 money supply, indexed to 2001 = 100

Every line goes up — that’s the point. Angle of attack tells the story.

All series matched through 2024; some central-bank sources lag a year or two.

EUR highlighted against the top 10 reserve currencies — M2 broad money, indexed to 2001 = 100. EUR series: ECB via DBnomics, as of 2026.

Euro M2 money supply

Broad money in EUR (cash + deposits + close substitutes), annual back to ~1960 via World Bank FM.LBL.BMNY.CN. Log scale auto-engages for hyperinflation outliers.

Euro inflation history

Annual CPI YoY since 1966 — World Bank consumer price index for Eurozone. Inflation volatility is one of three inputs into the Money2069 sound-money score.

{kind=link}

Purchasing power calculator

How much would your Euro be worth today if you'd held it since…?

Calculation: cumulative product of (1 + CPI YoY) from the chosen year through 2025. Source: World Bank consumer price index (annual). Daily-refreshed.

Data sources & methodology

- FX (USD):

- Frankfurter / ECB · daily, Exchange Rate API fallback

- CPI YoY:

- World Bank FP.CPI.TOTL.ZG · annual

- M2 broad money:

- IMF / central-bank monthly · World Bank annual fallback (LCU)

- Market cap (USD):

- M2 / FX rate · daily

- 10-year M2 change:

- (M2 today / M2 10y ago) − 1

- M69 score:

- Weighted: CPI (50%), 10y M2 growth (40%), 1y FX stability (10%)

- Last fetched:

- 2026-07-24 02:00:00

- Country code (ISO 3166-1):

- EMU

Note: 20-country currency union. World Bank Eurozone aggregate is empty for modern years; CPI/M2 via ECB direct feed in v2.

Raw data: /api/v1/currencies/current/EUR · Rates by Exchange Rate API

The Euro from a sound-money lens

20-country currency union, ECB-issued, 2% target — and missing it both ways.

The euro was born in 1999 as a political project as much as a monetary one — a single currency to bind together economies as different as Germany and Greece. Twenty-six years later, the experiment has survived a sovereign debt crisis (2010–12), a pandemic, and an energy shock — but at the cost of an ECB balance sheet that ballooned from €1T to over €8T at peak.

The European Central Bank targets "below but close to 2%" HICP inflation. In practice the post-2008 era saw years of sub-1% prints (Mario Draghi's "whatever it takes" QE era), then a sharp swing to over 10% in late 2022 as energy and supply shocks fed through. Both directions reveal the same fragility: a single monetary policy across 20 economies with structurally different inflation dynamics.

For savers, the euro's purchasing power has fallen meaningfully since launch. €100 in 2002 — when notes and coins entered circulation — is worth roughly €70 today in real terms. The ECB's broad money M3 has roughly tripled over the same window.

The euro's main soundness anchor is institutional: the ECB is, by treaty, the most independent of any major central bank, and the German Bundestag retains an unusual veto on transfers via the German constitutional court. Whether that holds under the next sovereign-debt stress is the open question — and the one Money2069 watches most closely.

Frequently asked questions

Who issues the Euro?+

What is the inflation rate of the Euro?+

Has the Euro been debased?+

Is the Euro sound money?+

How does the Euro compare to gold or the US dollar?+

How often is this data updated?+

Compare with

More from Money2069

The Euro inflates by policy. Money2069 runs on fixed rules — issuance targets 0%, purchasing power preserved by design, no central bank required.